What Are the Two Key Parties to a Promissory Note?

What are Notes Receivable?

Notes receivable are a balance canvas detail that records the value of promissory notes that a business is owed and should receive payment for. A written promissory note gives the holder, or bearer, the right to receive the amount outlined in the legal agreement. Promissory notes are a written promise to pay cash to some other political party on or before a specified future date.

If the note receivable is due within a twelvemonth, and then it is treated equally a current asset on the balance sheet. If it is non due until a engagement that is more than ane year in the futurity, so it is treated as a non-current nugget on the balance sheet.

Often, a business will allow customers to convert their overdue accounts (the business' accounts receivable) into notes receivable. By doing so, the debtor typically benefits by having more than time to pay.

Summary

- A annotation receivable is also known equally a promissory note.

- When the note is due within less than a year, information technology is considered a electric current nugget on the balance sheet of the company the note is owed to. If its due engagement is more than a year in the future, it is considered a not-current asset.

- The involvement income on notes receivable is recognized on the income argument. Therefore, when payment is made on a note receivable, both the balance sheet and the income argument are affected.

Key Components of Notes Receivable

Here are the key components of notes receivable:

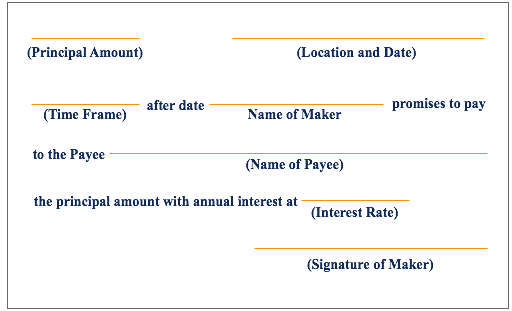

- Principal value: The confront value of the notation

- Maker: The person who makes the annotation and therefore promises to pay the annotation's holder. To a maker, the annotation is classified as a annotation payable.

- Payee: The person who holds the note and therefore is due to receive payment from the maker. To a payee, the notation is classified as a note receivable

- Stated involvement: A notation receivable generally includes a predetermined interest charge per unit; the maker of the note is obligated to pay the interest amount due, in addition to the principal amount, at the aforementioned time that they pay the principal amount.

- Timeframe: The length of fourth dimension during which the note is to exist repaid. Notes receivable are not normally subject to prepayment penalties, so the maker of the note is free to pay off the note on or before the note'due south stated due, or maturity, engagement.

Instance of Notes Receivable

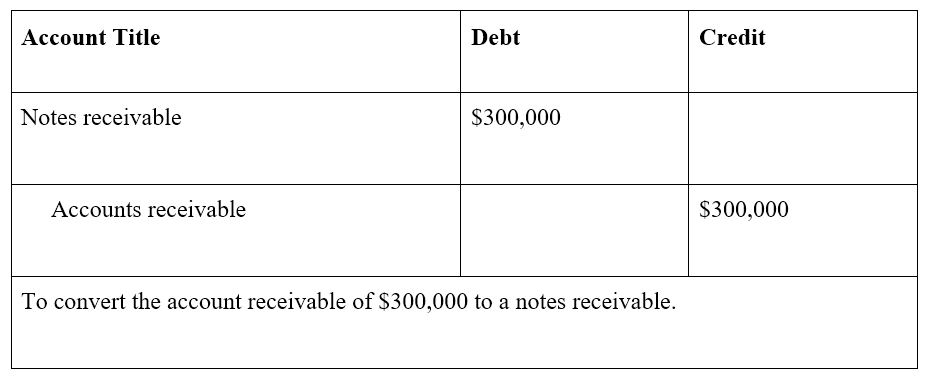

Company A sells machinery to Company B for $300,000, with payment due within 30 days. Later on 45 days of nonpayment by Visitor B, both parties agree that Visitor B will issue a annotation payable for the master corporeality of $300,000, at an interest rate of 10%, and with a payment of $100,000 plus interest due at the stop of each month for the side by side three months. Alternatively, the note may land that the total corporeality of interest due is to be paid along with the third and final principal payment of $100,000.

In this example, Visitor A records a notes receivable entry on its balance canvas, while Company B records a notes payable entry on its balance sheet. The principal value is $300,000, $100,000 of which is to be paid monthly. In improver, the agreed upon interest charge per unit on the note is x%.

Example of Journal Entries for Notes Receivable

Still using the example delineated above, with companies A and B:

A note receivable of $300,000, due in the adjacent three months, with payments of $100,000 at the end of each month, and an involvement charge per unit of 10%, is recorded for Company A.

The proper journal entries for Visitor A are every bit follows:

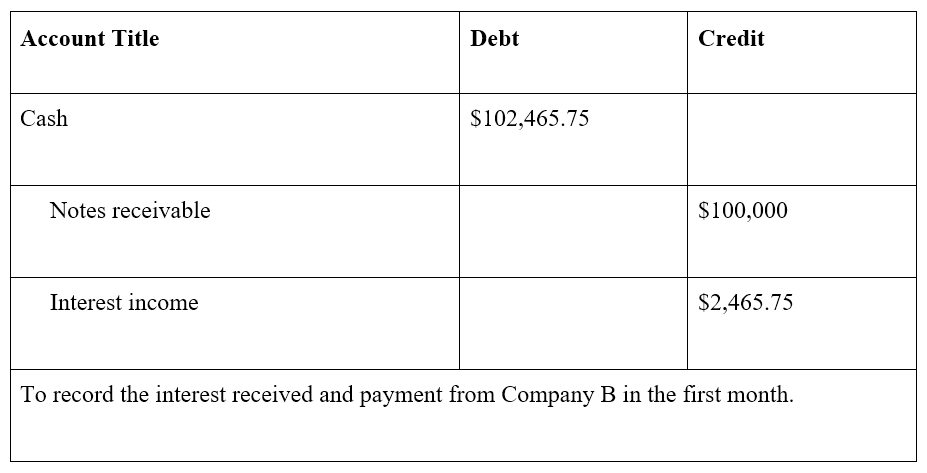

At the end of the first month, Visitor B pays $100,000 as well as an interest payment = $2,465.75 (calculated equally $300,000 x 10% x 30 / 365 days = $2,465.75).

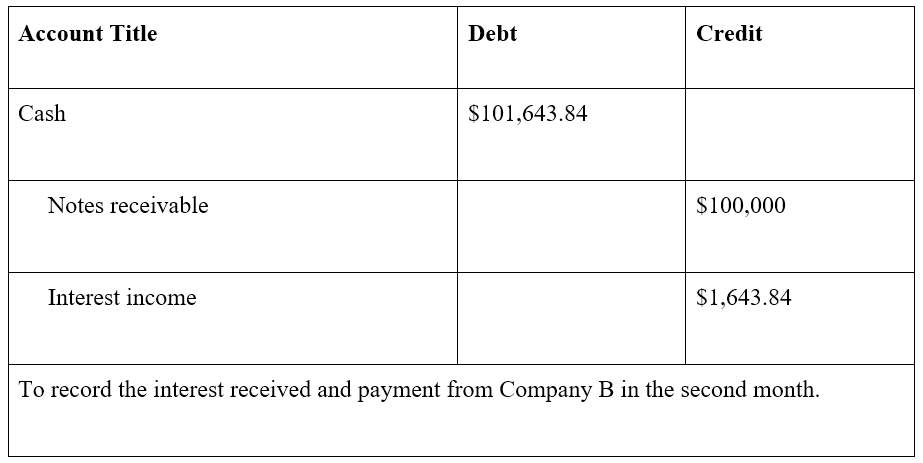

At the end of the 2d month, Company B pays $100,000, forth with interest of $200,000 10 10% x 30 / 365 days = $i,643.84. Note that the corporeality of involvement is lower because the outstanding principal corporeality is at present simply $200,000 ($300,000 – $100,000), having been reduced past the previous month's payment.

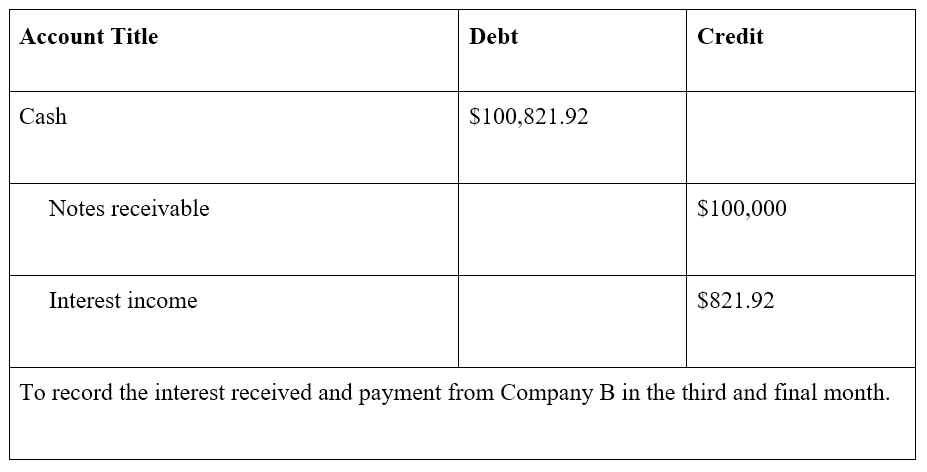

At the end of the third and terminal calendar month, Company B pays the remaining principal of $100,000, as well as the interest of $100,000 10 ten% x 30 / 365 days = $821.92

At the end of the three months, the note, with interest, is completely paid off.

Notes Receivable vs Notes Payable

It is non unusual for a company to accept both a Notes Receivable and a Notes Payable account on their statement of fiscal position . Notes Payable is a liability equally it records the value a business concern owes in promissory notes. Notes Receivable are an nugget as they record the value that a business is owed in promissory notes. A closely related topic is that of accounts receivable vs. accounts payable.

Additional Resources

Thanks for reading our guide to Notes Receivable. CFI's mission is to help anyone in the world become a world-class financial annotator through completing the Fiscal Modeling & Valuation Analyst (FMVA)® credential plan. To continue learning and advancing your career in corporate finance, y'all may notice the additional costless CFI resources below helpful:

- Sales and Collection Cycle

- Accounts Payable

- Projecting Residuum Sheet Items

- Three Financial Statements

Source: https://corporatefinanceinstitute.com/resources/knowledge/accounting/notes-receivable/

0 Response to "What Are the Two Key Parties to a Promissory Note?"

Post a Comment